The BDC Reporter is kicking off a new series for all readers: BDC Preview. Our goal is to provide a heads up at the beginning of every week of what lie ahead for anyone interested in the Business Development Company sector.

MARKET REBOUND: The BDC sector rebounded in the week November 2, 2018 after 5 weeks of decline. That slump put an end to a 7 month BDC rally, and brought the YTD sector price 10% below the level at December 29, 2017. At its current level, the BDC sector is 23% off its March 2017 high and 31% off its 2013 All Time High. Or, to put matters another way, there’s plenty of upside despite the 3.0% upside move last week. However, what with the unsettled major markets, the mid-term elections and Week Two of BDC earnings season this could go any number of ways: up, down or sideways.

EARNING SEASONS- EPISODE TWO: Last week 11 BDCs reported earnings. Much as we anticipated there were no disasters, either in terms of profits or credit quality. In fact, there were several BDCs that reported results ahead of expectations, including market leader Ares Capital (ARCC), as well as technology BDC Horizon Technology Finance(HRZN). Both were rewarded with higher stock prices ahead of the sector increase. ARCC was up 6.3%, but was as much as 6.9% up intra-week. HRZN closed the week 10.7% higher than the Friday before.

This week a monumental 22 BDCs – according to our BDC Earnings Calendar – will be coming out with their latest results. By the time that’s done, and after including MVC Capital (MVC) and Saratoga Investment (SAR) which have earlier in the quarter closing periods, 35 of the 45 BDCs we track will have reported. After that shareholders get a respite (except for OHA Investmenti.e. OHAI) till BDCs with year-ends in September file their 10-Ks, mostly scheduled for the last week of November.

With so much going on here are some of the BDC releases worth focusing on:

November 5: Capitala Finance (CPTA) – in the middle of a strategic repositioning after a host of bad loans and two dividend cuts in a short period – will be worth watching. Key question: What progress has the BDC made in selling off/down equity stakes to re-invest in yielding loan investments ? We’ve been hopeful that this approach might help the BDC stabilize and eventually grow earnings. However, CPTA has not been publicly mentioning any individual successes in recent weeks. Maybe the program is stalled and/or is being offset for the moment by further credit problems. These turnarounds – if they happen at all – take multiple quarters to play out, so this period’s results will only be a way station on the way to CPTA’s ultimate stabilization or another dividend cut.

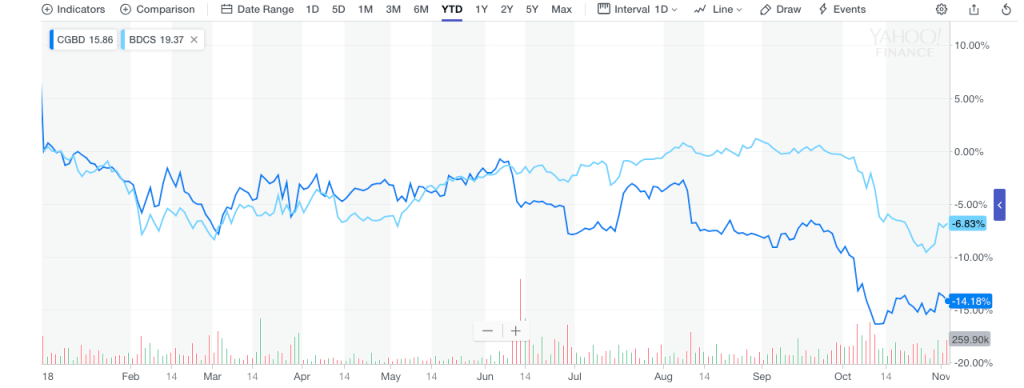

November 6, 2018: For reasons not entirely clear to the BDC Reporter – or many of its shareholders- the Carlyle Group’s BDC – TCG BDC with the ticker CGBD – has been declining in price all year, and at more than twice the pace of the sector as a whole:

Currently, this recent addition to the public markets trades at a (12%) discount to book value.

The third quarter earnings release may provide some insight into why this BDC with a famous parent is faring so poorly. We’ll be looking for credit troubles bubbling to the surface – which the market may have picked up on early.

Or, perhaps, the anticipation that the former shareholders of CGBD when private might seek to register and sell their shares caused the price to drop.

On October 25, 2018, though, the BDC announced in a dry filing – and without issuing a press release, the following:

As previously disclosed, TCG BDC, Inc. (the “Company”) is required to initiate certain registered underwritten secondary offerings on behalf of its pre-initial public offering (“IPO”) investors following the Company’s IPO pursuant to the terms of the subscription agreements entered into by the Company and its pre-IPO investors (the “Subscription Agreements”). Accordingly, the Company delivered a written notice to its pre-IPO investors to offer such investors the opportunity to participate in a registered underwritten secondary offering (the “Proposed Secondary Offering”). Because the aggregate commitments to sell in the Proposed Secondary Offering did not meet the minimum offering size required under the Subscription Agreements, the Company notified investors on October 25, 2018 that the Company would not be proceeding with the Proposed Secondary Offering.

We may learn more from CGBD’s Conference Call or not, as BDCs can be evasive or tight lipped about such things.

Merger Blues

November 7, 2018: Speaking of big name BDCs taking a price shellacking…Both FS Investment(FSIC) and Corporate Capital Trust (CCT) have been dropping like rocks since August on the news of their imminent merger.

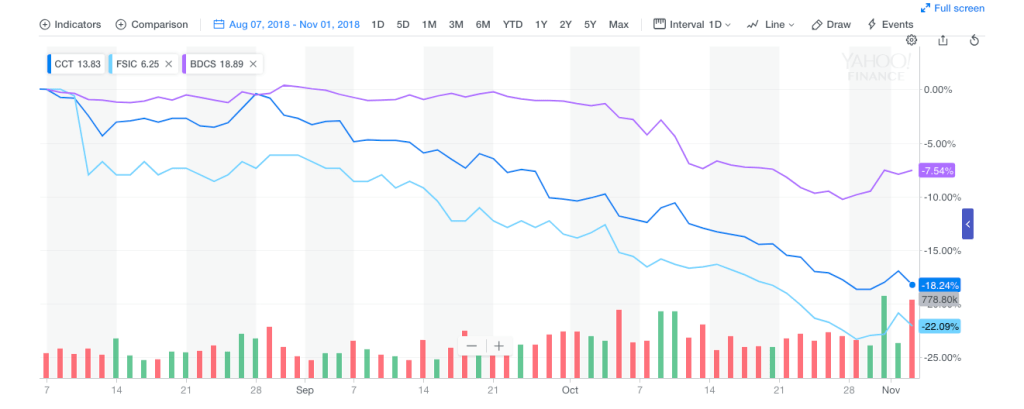

Just take a look at this chart from August 7 to November 1, 2018 :

FSIC – formerly run along with the FS Investments Group by GSO Blackstoneand now a partnership between the former and KKR – is down over (20%), three times worse than BDCS in the same period.

This is not an auspicious start for KKR-FS Investments, and begs the question why ?

Maybe the portfolio at FSIC left by GSO Blackstone – despite an apparently amiable hand off between the two firms – was not as in good shape as the Investment Advisor has led investors to believe ?

Or else FSIC shareholders may not be enamored – when pen is put to paper – by the exchange ratio offered CCT shareholders for merging into their BDC.

CCT itself also has a loan portfolio with many question marks.

On November 7, we’ll learn more about the credit situation at both BDCs, shortly before they merge into one of the largest players out there.

We may also get the promise of a grand gesture by the co-Investment Advisors to boost the stock price, such as a major stock buy-back program.

Nothing Succeeds Like Credit Success

Long term, though, FSIC will have to demonstrate that it has the credit skills to match other BDC giants like ARCC.

If FSIC traded at book value – which ARCC does as of November 2, 2018 – its stock price would be 44% higher.

Big Picture

Of course every BDC quarterly earnings provides us with some new information and much more than what we learn through the rest of the period.

We’ll be reviewing each press release; investor presentation, quarterly filing and Conference Call transcript for meaningful developments not already well known.

On a broader scale – based on what we’ve been gleaning from random comments and disclosures in Week One – we’ll be keeping an eye out on what BDCs have to say about the impact of tariffs on portfolio companies.

To date, the Trump tax cuts do not appear to have had much impact on BDC portfolio company performance or valuations.

However, we’re repeatedly hearing that some BDC portfolio companies might be beginning to be impacted by the tariff wars underway.

BDCs are understandably being very careful about what they say, but we suggest readers keep attuned to the subject.

Portfolio companies of BDCs – which have been enjoying multi-year increases in sales and EBITDA – are now facing pressures on margins from tariffs; higher fuel costs and over a year of ever increasing LIBOR.

BlackRock Capital (BKCC) went so far as to add this risk disclosure in its latest 10-Q:

Changes to United States tariff and import/export regulations may have a negative effect on our portfolio companies and, in turn, harm us.

There has been ongoing discussion and commentary regarding potential significant changes to United States trade policies, treaties and tariffs. The current administration, along with Congress, has created significant uncertainty about the future relationship between the United States and other countries with respect to the trade policies, treaties and tariffs. These developments, or the perception that any of them could occur, may have a material adverse effect on global economic conditions and the stability of global financial markets, and may significantly reduce global trade and, in particular, trade between the impacted nations and the United States. Any of these factors could depress economic activity and restrict our portfolio companies’ access to suppliers or customers and have a material adverse effect on their business, financial condition and results of operations, which in turn would negatively impact us.

A Little Bad News Goes A Long Way

Of course, many portfolio companies will not be affected – even indirectly – by tariffs, but it takes financial pressure on only a fraction of the BDC borrowing universe to cause enough defaults to have a material impact on investor returns.

Just remember what exposure to a relatively small number of energy credits in a relatively small number of BDCs in 2014-2016 did to sector and individual stock prices.

Chances are the first cracks in the U.S. economy will show up amongst the most leveraged companies.

The BDC sector – with its exposure to over 3,000 mostly private companies, all of whom are leveraged – is the canary in the credit coal mine.

As the BDC Reporter and investors generally pore over earnings one or two cents higher or lower than expectations it’s worth keeping an eye at what we might be able to make out coming down the pike.

Is that an ever improving economy or something more sinister ?

In this highly cyclical business getting the answer right can be critical

.png)