Curiouser And Curiouser

Week Two of 2018 for BDC common stocks was a little strange.

Flooded

First, there was a burst of news activity. The BDC News Of The Day listed 29 separate developments, not including our Stock Watch updates or earning release announcements.

Where there is news, there is often market movement.

All Over

Second, there were a lot of downs and ups where BDC prices were concerned.

For example, 41 of 46 BDCs were up on Friday but earlier in the day BDCS (the Exchange Traded Note which covers the group) was at its lowest level in over a year, and lower than the prior low point in 2017.

[BDCS ended at $20.41, down from $20.77]Down Below

Likewise, during the week several well regarded names reached or almost reached 52 Week Lows.

TCPC, FDUS, ARCC and GBDC were amongst those “testing their lows”.

Change

Then – as if a bell went off (or an algorithm) investors plunged in – on some names – and boosted up the price by week’s end.

The BDC Reporter likes to track intraday how many BDCs are within 5% and 5%-10% of their 52 Week Low as a proxy for market sentiment.

Through most of the week the count was high and going higher, reaching 19 names just in the 0%-5% off the low category.

By Friday’s close, though, that was down to 13. There were another 14 in the 5%-10% group.

For The Week

On the week as a whole- according to Seeking Alpha data – only 7 BDCs were down on the week, two were flat and 37 were up.

As of Friday 19 BDCs were trading above their 50 Day Moving Average and 27 below. On the 200 Day scale the picture is more clear cut: only 10 are trading above.

Specifically Speaking

There were four BDCs which increased in price more than 3% on the month.

Most of all there was MFIN – in the midst of a dramatic market re-evaluation: up a remarkable 37%, and breaking price records.

Then there was TCAP which was 8.0% up , benefiting from an analyst call.

OHAI was up 4.4% on no news, but its thinly traded status can exacerbate both ups and downs.

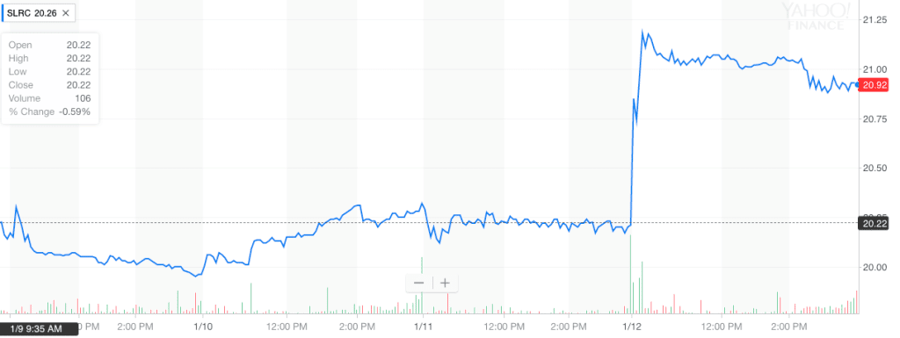

SLRC was up 3.8%, but only thanks to a last minute market enthusiasm, as this 5 Day chart illustrates.

No Downers

No BDC stock moved more than 3% down on the month, but we couldn’t help noticing that NEWT‘s price continued to erode after reaching new heights late last year.

NEWT peaked at $19.20, but is now back at $17.77.

DIVIDEND OUTLOOK

The BDC Reporter recorded a second change on the year in its view about the odds of dividend sustainability for a BDC in the year ahead.

Last week, we downgraded our view for CPTA from UNCHANGED to AT RISK. In that case, we were only catching up with the market which – using the 13.1% yield as our guide – appears to be doubtful about the $1.0 a year payout.

This week – while reviewing GECC‘s new Unsecured Notes and the accompanying Prospectus, we changed our view to DECREASE from UNCHANGED.

By our lights, the conversion of a large portion of Avanti Communications debt (GECC’s biggest investment by far) to equity will cause earnings and distributions to drop.

Then there is the cost of not one but two expensive Unsecured Notes. That interest bill will have to be paid before the new capital raised will get deployed and earnings its keep.

The market seems comfortable with the risk as GECC yields 9.7% (16% below NAV). We are either early or wrong…

That leaves the BDC Reporter’s Dividend Outlook scorecard for 2018 with 26 UNCHANGED, 14 AT RISK and 6 in the DECREASE category.

Coming Up

The BDC sector is already getting ready for IVQ 2017 earnings results.

This week we added ever more names to the BDC Earnings Calendar (see the Tools section on the front page). The first releases start on February 6.

[This week SAR reported in-line results, but that was for its fiscal third quarter ended November 2017.However, each BDC spins market conditions differently so we’ll have to see].

Not Very Controversial

With the outlook for a host of BDCs up in the air (we count 24 in some sort of transition), the BDC Reporter expects we may see more price volatility ahead.

More So

Given that we believe the prospects of most BDCs are to the downside, the trend is likely to be lower over the medium term.

To our mind, investors remain a little too optimistic despite a (15%) drop in BDCS since March 2017.

In the last 52 weeks 31 of 46 BDC prices – drawn from Seeking Alpha’s data – have moved lower.

We don’t see why that wouldn’t continue with many BDCs loaded up with troublesome loans; higher borrowing costs from LIBOR and the benefits of floating rate loans being offset by spread compression.

Many BDCs are covering their distributions only by temporarily waiving fees and by booking large chunks of Pay In Kind Income (GECC admits 46% of its Investment Income was in PIK form).

We’d be happy to be proven wrong, but we expect more Bad News Than Good News in the weeks ahead.

The BDC Reporter will be on the frontlines to alert our readers one way or the other.

FIXED INCOME

Like The Arctic

For the week, the 34 BDC Fixed Income issues we track dropped in median price to $25.43 from $25.54.

That’s only a (0.4%) weekly decrease.

Moreover, all the metrics we usually trot out are essentially the same:

There is only 1 issue trading below $25.00 (CPTAG) and 1 over $26.00.

However, we expect the median price to melt like the ice caps – slowly, invisibly to the naked eye.

Under Pressure

First there is the recent rise in medium term rates, which places pressure on existing debt prices.

Then – as we discussed at great length last week – there is the uncertainty surrounding more than half the issues about early redemption in 2018.

With every passing week, the question marks over many names rises.

This week the two Oaktree run issues OCSLL and OSLE as well as Medley’s MCV and Hercules Capital’s HTGX all closed at prices less than 10 cents off par.

Twofer

Still, this week was notable for two new BDC fixed income issues.

The largest BDC – and a multiple Unsecured Note issuer – ARCC borrowed $600mn till 2025 at a rate of 4.25%.

That wasn’t the lowest rate ARCC has ever been able to achieve, but remains one of the best for 7 year paper.

The capital was raised from institutional investors and will not trade with a public ticker.

Then one of the smallest BDCs- but also a multiple Unsecured Note issuer – GECC also issued a 7 year Baby Bond.

This does have a ticker : GECCM and was just priced at a coupon of 6.75%, and will raise up to $50mn for GECC.

The BDC Reporter wrote a long article about GECC’s second Baby Bond since September 2017 which will be interesting to both common stock and debt investors in the fund.

Updating

We’ve not yet fully updated the Fixed Income Table because GECCM is still trading in the “grey market”.

However, by this time next week we expect to have the number of public BDC issues back up to 35 when GECCM takes its rightful place on our list.

Range Bound

For everybody else, the two issues provide an illustration of what the book-ends are for 7 year unsecured debt for most every BDC issuer: somewhere between 4.25% and 6.75%.

If we get a rush of BDC issuers trying to raise debt before the cost rises with higher rates there may be more Unsecured Notes coming to market than we’ve anticipated.

That might help to mitigate (unlikely to reverse) the slight shift downwards in median public BDC Fixed Income prices.

.png)