Primary market yields on first lien middle market loans rose to their highest levels since Q1 2017 with increases in each quarter of 2018. This movement was driven heavily by the steady increase in LIBOR of over 100 bps throughout the year along with modest increases in coupon spread, most notably in the fourth quarter. First and second lien coupon spreads widened 35 and 33 bps respectively in the quarter, marking the largest quarterly spread widening in 2 years.

Read More

Topics:

Loans,

Middle Market,

Analytics,

market analytics,

Fixed Income,

download,

research

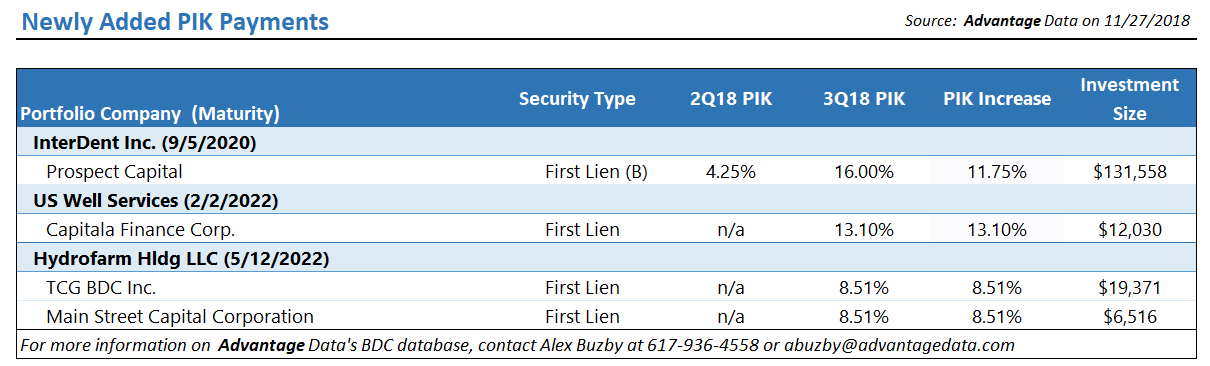

Analyzing PIK and Coupon Spread changes can be a great way to identify middle market companies that are beginning to feel pressure from lenders. Whether you're sourcing investments, consulting distressed borrowers or analyzing BDCs, utilizing alternative signs of distress as leading indicators is a great way to get ahead of the market - Download the data sample below!

Read More

Topics:

Middle Market,

BDC,

Spreads,

First Lien,

Distressed Investments,

debt,

business development company,

Distress,

Distressed Debt,

Finance,

Restructuring,

Fixed Income,

download

Even in markets where established data infrastructure is limited, such as syndicated loans, reliable sources of data that are indicative of a liquid security’s value are available through market data vendors and broker quotes. When evaluating illiquid securities like middle market or directly originated loans, the effort of data aggregation becomes much more difficult and is often assumed to be an exercise in futility. We would disagree.

Read More

Topics:

Loans,

Middle Market,

BDC,

business development company,

Valuation,

Fixed Income,

illiquid,

download,

Direct Lending,

syndicated

A quarter over quarter coupon spread increase can be an early warning sign for investors and restructuring advisors that the issuer may be facing financial troubles.

What do we mean by “coupon spread increase”? First, the coupon is simply the annual interest payment paid by the issuer relative to the loan or bond's face or par value. Coupon spreads compare the interest rate differential between two loans or bonds. Say the coupon rate is 5% in the first quarter of the year, and then changes to 7% the next quarter. This would cause a coupon spread increase between it and the coupon of a comparable loan or bond. [source]

An increased coupon spread from one quarter to another is an indicator that something happened – it does not mean there is imminent risk of default. If a company does not meet its obligation to its lenders, it may be required to take some sort of action to make good on its promises of repayment or otherwise remain in good faith. One such action could be an increase of the coupon payment.

Read More

Topics:

Loans,

BDC,

Distressed Debt,

Restructuring,

download

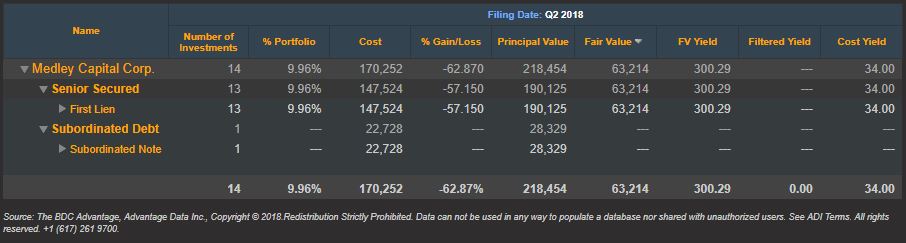

Last month we shared a list of the top 10 BDC non-accruals based on first quarter 2018 SEC filings. Now that we are mid-way through August and second quarter filings are readily available, let’s take a fresh look at the first quarter’s worst performer.

Read More

Topics:

BDC,

First Lien,

Non-accruals,

Distressed Debt,

Restructuring,

Second Lien,

Loan Default Rate,

BDC Filings,

Default Rate,

Fixed Income,

fair value,

portfolio,

download,

News

.png)