BOND INVESTORS TURN BEARISH on longer-dated U.S. government debt following the release of asound June payroll report and reducing bets the Fed will cut interest rates this month. Analysts say a prolonged inverted yield curve is a predictor of a recession and has foreshadowed the last nine recessions. “It has to stay there for a couple of months before you start to worry. One month or so, we wouldn’t consider it a lengthy period of time,” said Falconio. “We believe it’s an indicator of a long-term recession, however, it isn’t signaling a recession any time soon.” The spread between the two and ten-year notes narrowed to 14.2 basis points, the closest since May 31st. The 10-year note advanced 0.8 basis points. S&P +0.12%, DOW -0.08, NASDAQ +0.54%

JOB OPENINGS SLIGHTLY FELL to 7.32 million remaining near record highs as companies hired 5.73 million people in May. Hiring

dwindled in the manufacturing and heavy-industry sectors largely due to the ongoing trade spat between the U.S. and China. Openings outnumber the number of unemployed for the

fifteenth straight month as employers struggle to find skilled labor.

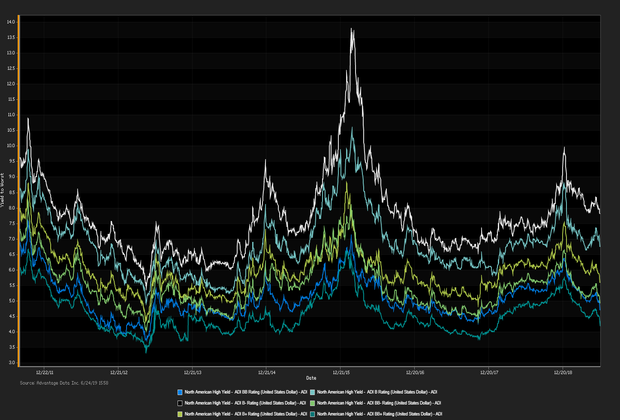

ADI proprietary index data showed a net

yield increment for high-yield versus high-grade bonds. High-grade edged out high-yield. Among high-grade bonds showing topmost price gains at appreciable volumes traded,

Transcontinental Gas Pipe Corp. (USD) 5.4% 8/15/2041 made analysts' 'Conviction Buy' lists. (See the chart for

ADI Indices above.)

Corey Mahoney (

cmahoney@advantagedata.com).

| Key Gainers and Losers |

Volume Leaders |

| + |

Pacific Gas & Electric Co. 6.05% 3/1/2034 |

+ 2.3% |

| |

Western Digital Corp. 4.75% 2/15/2026 |

+ 0.1% |

| - |

US Steel Corp. 6.875% 8/15/2025 |

-0.5% |

|

United States STL Corp. New 6.25% 3/15/2026

Mednax Inc. 5.25% 12/1/2023 Reg S

|

| Industry Returns Tracker |

| Industry |

Past Day |

Past Week |

Past Month |

Past Quarter |

YTD |

Past Year |

| Agriculture, Forestry, Fishing |

-0.04% |

0.26% |

5.25% |

5.82% |

12.31% |

14.64% |

| Mining |

-0.16% |

-0.38% |

0.58% |

-1.49% |

7.46% |

2.25% |

| Construction |

-0.04% |

-0.10% |

1.61% |

3.37% |

11.07% |

9.26% |

| Manufacturing |

-0.02% |

-0.02% |

1.55% |

2.20% |

9.33% |

7.93% |

| Transportion, Communication, Electric/Gas |

-0.01% |

-0.11% |

1.75% |

3.26% |

10.23% |

9.42% |

| Wholesale |

-0.08% |

0.00% |

1.74% |

2.88% |

10.36% |

7.93% |

| Retail |

0.03% |

-0.12% |

1.66% |

3.78% |

12.35% |

9.63% |

| Finance, Insurance, Real-Estate |

-0.05% |

-0.04% |

1.65% |

2.72% |

10.21% |

9.61% |

| Services |

-0.02% |

-0.12% |

1.27% |

2.50% |

10.02% |

9.41% |

| Public Administration |

-0.18% |

0.43% |

2.29% |

3.69% |

9.92% |

14.01% |

| Energy |

-0.15% |

-0.34% |

0.60% |

-0.49% |

7.84% |

2.80% |

| |

| Total returns (non-annualized) by rating, market weighted. |

|

| New Issues |

Forward Calendar |

|

(None Current 07/09/2019)

|

1. Atlantica Tender Drilling Ltd: $140MM, Expected Q3 2019

2. Alpha Auto Group: $225MM, Expected Week of 6/24

|

Additional Commentary

NEW ISSUANCE WATCH: on 7/2/19 participants welcome a $243MM new corporate-bond offering by AAG FH LP/AAG FH Finco Inc. The most recent data showed money flowed out of high-yield ETFs/mutual funds for the week ended 6/21/19, with a net outflow of $602MM, year-to-date $8.9B flowed into high-yield.

| Top Widening Credit Default Swaps (CDS) |

Top Narrowing Credit Default Swaps (CDS) |

Hovnanian Enterprises Inc. (5Y Sen USD XR14)

Controladora Mabe SA de CV (5Y Sen USD CR14) |

San Miguel Corp. (5Y Sen USD CR14)

Atmos Energy Corp. (5Y Sen USD MR14) |

Loans and Credit Market Overview

SYNDICATED LOANS HIGHLIGHTS:

Deals recently freed for secondary trading, notable secondary activity:

- Piaggio & C. SpA, Goshawk Aviation Ltd, Valence Surface Technologies

OVERALL CREDIT MARKET:Long-term bond yields are expected to hit a cyclical peak in 2019 given tight fiscal policy and lagging global economies. Europe remains checked by stubbornly low inflationary forces. Positive effects remained in force:

- TED spread held below 11 bp (basis points), as of 07/09/19

- Net positive capital flows into high-yield ETFs & mutual funds

Copyright 2019 Advantage Data Inc. All Rights Reserved. http://www.advantagedata.com

Information in this document should not be regarded as an offer to sell or solicitation of an offer to buy bonds or any financial instruments referred to herein. All information provided in this document is believed to be accurate. However, Advantage Data and its sources make no warranties, either express or implied, as to any matter whatsoever, including but not limited to warranties of merchantability or fitness for a particular purpose. Opinions in this document are subject to change without notice. Electronic redistribution, photocopying and any other electronic or mechanical reproduction is strictly prohibited without prior written permission from Advantage Data Inc.

.png)