ATTENTION WILL FOCUS ON THE FED’S two-day meeting this week concluding with a monetary policy statement on Wednesday. A recent survey indicated 40 percent of economists polled expect the Fed to ease economic policy next month. Over the past 30 days, the 10-year note fell 45 basis points following tariff uncertainties and slowing economic data. The 10-year note held steady losing 0.4 basis points. Gold slips from 14-month highs, however, continues to see significant inflows as investors flee to the safe-haven asset. S&P +0.16%, DOW +0.15, NASDAQ +0.69%.

VOLATILITY IN THE BOND MARKET SURGES to levels not seen in nearly 3-years amid the recent soft employment report. Tom di Galoma managing director at Seaport Global Securities stated

, “Bond markets are seeing something that equity markets are not”. The manufacturing confidence in New York tumbled into negative territory recording the

largest drop ever plummeting 26.4 points. Economists

“raise the caution flag” that other manufacturing data may come in weaker than expected this month as the

imposing tariffs take a toll on the economy. ADI proprietary index data showed a net

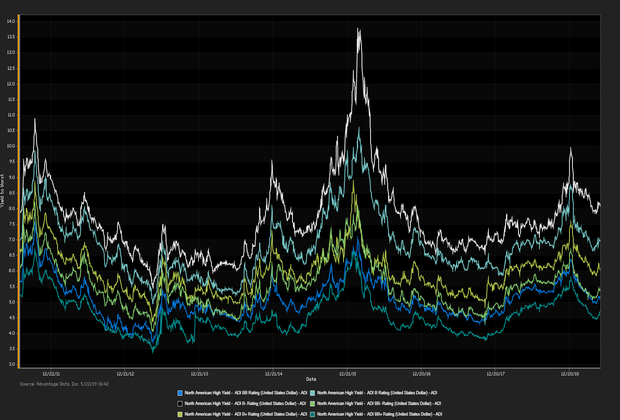

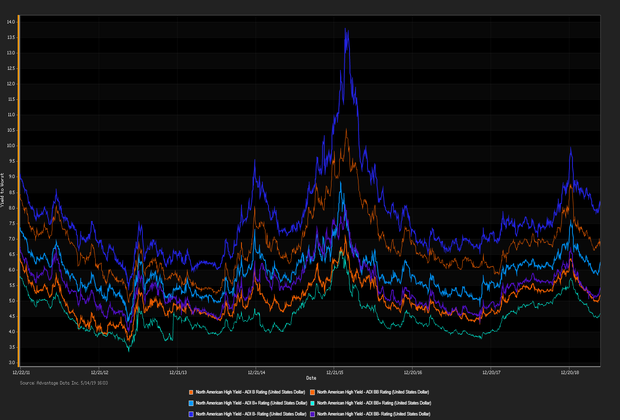

yield increment for high-yield versus high-grade bonds. High-grade edged out high-yield. Among high-grade bonds showing topmost price gains at appreciable volumes traded,

Canadian Pacific Railroad Co. (USD) 4.8% 8/1/2045 made analysts' 'Conviction Buy' lists. (See the chart for

ADI indexes

above.)

Corey Mahoney (

cmahoney@advantagedata.com).

| Key Gainers and Losers |

Volume Leaders |

| + |

Alliance One Intl Inc. 9.875% 7/15/2021 |

+ 0.2% |

| |

MGM Growth Properties Operating Partnership LP 5.625% 5/1/2024 |

+ 0.2% |

| - |

Hertz Corp. 5.5% 10/15/2024 Reg S |

-0.5% |

|

Teva Pharmaceuticals Fin BV 6.75% 3/1/2028

HCA Inc. 6.5% 2/15/2020

|

| Industry Returns Tracker |

| Industry |

Past Day |

Past Week |

Past Month |

Past Quarter |

YTD |

Past Year |

| Agriculture, Forestry, Fishing |

0.28% |

1.29% |

2.86% |

4.99% |

10.43% |

12.93% |

| Mining |

-0.17% |

-0.43% |

-2.26% |

-0.68% |

6.39% |

1.03% |

| Construction |

-0.03% |

0.34% |

1.26% |

3.90% |

9.11% |

6.73% |

| Manufacturing |

-0.05% |

0.32% |

0.53% |

2.04% |

7.94% |

5.98% |

| Transportion, Communication, Electric/Gas |

-0.04% |

0.10% |

1.31% |

3.10% |

8.68% |

7.32% |

| Wholesale |

-0.00% |

0.45% |

1.26% |

2.89% |

9.39% |

5.85% |

| Retail |

-0.04% |

0.50% |

1.21% |

4.32% |

11.33% |

7.71% |

| Finance, Insurance, Real-Estate |

-0.01% |

0.35% |

1.03% |

2.67% |

8.91% |

8.01% |

| Services |

-0.07% |

0.32% |

1.43% |

2.81% |

9.11% |

7.74% |

| Public Administration |

-0.08% |

0.74% |

1.47% |

2.43% |

8.25% |

13.11% |

| Energy |

-0.16% |

-0.46% |

-2.18% |

-0.63% |

6.16% |

0.70% |

| |

| Total returns (non-annualized) by rating, market weighted. |

|

| New Issues |

Forward Calendar |

|

(None Current 06/17/2019)

|

1. Q'Max Solutions Inc.: $225MM, Expected Week of 6/17

2. Obsidian Energy LTD: $100MM, Expected Week of 6/17

3. Petroleum Geo-Services: $150MM, Expected Week of 6/17

|

Additional Commentary

NEW ISSUANCE WATCH: on 6/13/19 participants welcome a $500MM new corporate-bond offering by Harsco Corp. The most recent data showed money flowed out of high-yield ETFs/mutual funds for the week ended 6/14/19, with a net inflowof $1.7B, year-to-date $8.3B flowed into high-yield.

| Top Widening Credit Default Swaps (CDS) |

Top Narrowing Credit Default Swaps (CDS) |

Hertz Corp. (5Y Sen USD XR14)

Hovnanian Enterprises Inc. (5Y Sen USD MR14) |

Cable & Wireless Communication (5Y Sen USD CR14)

SuperValu Inc. (5Y Sen USD MR14) |

Loans and Credit Market Overview

SYNDICATED LOANS HIGHLIGHTS:

Deals recently freed for secondary trading, notable secondary activity:

- US Renal Care Inc., Perforce Software Inc., Avantor Performance Materials Inc.

OVERALL CREDIT MARKET:Long-term bond yields are expected to hit a cyclical peak in 2019 given tight fiscal policy and lagging global economies. Europe remains checked by stubbornly low inflationary forces. Positive effects remained in force:

- TED spread held below 23 bp (basis points), as of 06/17/19

- Net positive capital flows into high-yield ETFs & mutual funds

Copyright 2019 Advantage Data Inc. All Rights Reserved. http://www.advantagedata.com

Information in this document should not be regarded as an offer to sell or solicitation of an offer to buy bonds or any financial instruments referred to herein. All information provided in this document is believed to be accurate. However, Advantage Data and its sources make no warranties, either express or implied, as to any matter whatsoever, including but not limited to warranties of merchantability or fitness for a particular purpose. Opinions in this document are subject to change without notice. Electronic redistribution, photocopying and any other electronic or mechanical reproduction is strictly prohibited without prior written permission from Advantage Data Inc.

.png)