Last week’s look at BDC non-accruals showed an overall rate that still ran below historical norms, but what about the lower middle market? All BDCs invest in these names —that’s the nature of the business— but some drill down more than others.

In order to isolate LMM loans from larger credits, Direct Lending Deals looked only at BDCs that explicitly stated an investing strategy of “lower middle market” or that targeted an issuer size of less than $30M of EBITDA. Needless to say, it was not a simple exercise, nor an exact science for several reasons.

First, many BDCs still do not define middle market, much less the lower middle market, nor is there consistency across the ones that do. Some managers call issuers with $15M to $100M of EBITDA middle market. Others have a narrower range: $5M to $50M of EBITDA. The variations are countless, based on EBITDA, revenue or enterprise value.

DL Deals found nine managers that specified our parameters across eight portfolios. This group manages $2.1 billion in debt investments — those being first-lien, second-lien or unitranche. That pales in comparison to the $78 billion of similar investments across all BDCs, per Advantage Data’s BDC database.

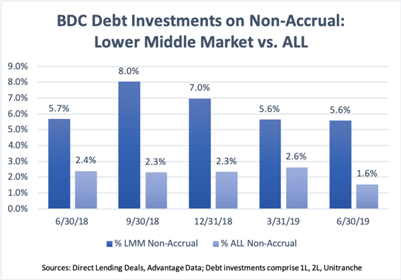

Within this small circle, the non-accrual rate was 5.6% compared to 1.6% for all BDCs, as of June 30. In the year ago period, LMM non-accruals were 5.7% compared to 2.4% overall. (The math is cost basis.)

Beyond the thin data challenges, other complexities make a clean dissection difficult. Large and small borrowers go into non-accrual in different ways and for different periods of time.

Larger companies will navigate Chapter 11 more quickly because they have deeper pockets and more lawyers, and suddenly return as a “performing” credit. They also can pull more levers to avoid or get out from a non accrual state. That makes the non-accrual numbers look better, but there is a long term or permanent loss of income, and whatever problems existed have not magically disappeared.

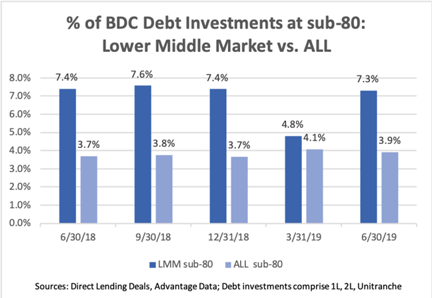

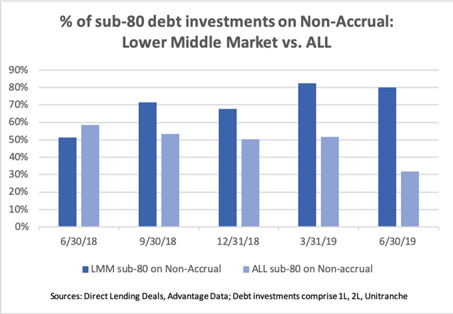

A similar gap can be seen across underperformers valued at less than 80, with LMM credits having a much higher rate in all but one of the past five quarters. Here, too, there are nuances to be noted.

Marking to market a LMM investment is truly an art form since there is no real secondary trading to speak of and 99.9% are private borrowers with few, if any, transparent comps. Some managers may take a realistic approach; others are more forgiving.

Although limited in scope, the data in this set supports a long-held belief that small businesses will have a tougher time navigating prolonged volatility than larger ones. A $100M EBITDA business, for example, should be able to better withstand a storm than, say, a $5M EBITDA company.

Investors argue, however, that smaller companies typically find the lender, or club of lenders, more flexible in solving issues. Depending on the financial sponsor, equity cures can be easier to procure as well. A $5M band-aid can be easier to administer than a $500M blood infusion.

No matter the spin, when the 10-year expansion cycle breaks, the biggest factor hanging over any portfolio is the manager. —Kelly Thompson

kelly.thompson@dldeals.com; (773) 954-8207

Mark O’Brien: mobrien@advantagedata.com; (617) 936-4556

********Coming soon! Direct Lending Deals is a new publication that lifts the curtain on private credit by giving investors and originators the latest news and analysis on terms & trends in the direct lending market, now a $1 trillion dollar asset class. DL Deals focuses on sponsor-driven transactions, the main engine of deal flow in leveraged lending. We tap into 20-year relationships to go deeper on deals, and cover all segments of direct lending including fundraising, BDCs and people shaping the market. Contact kelly.thompson@dldeals.com to join the DL Deals distribution list. Website and formal launch coming next month.********

.png)