BDC COMMON STOCKS

Yoked Together

Another week and another instance of the BDC sector being synced to the S&P. Or so the numbers seem to show.

For the week, the S&P 500 index was up 0.54%. The UBS Exchange Traded Note which owns most of the publicly listed BDCs – ticker BDCS – was up 0.52%. In the approach to earnings season, there’s little else that can move the BDC sector, so why not?

Higher

Most of the 46 BDCs we track were up in price: a relatively high 38.

However, there were only three up by 3.0% or more, suggesting more of a general calm than a great leap forward.

There was only one BDC that dropped (3.0%) or more.

You Know Who

That was Medley Capital (MCC), which announced that no buyer had been found after weeks of rooting around by its financial adviser.

The BDC Reporter discussed and analyzed the news on October 15, 2019 minutes after the announcement.

(Bit of a setback for Houlihan Lokey who was doing the leg work, but we can’t judge fairly given the paucity of information about how the sales offer was presented and evaluated).

MCC is down (12.8%), to close at $2.24, not far from its 52 week low.

Whether that continues depends on what happens next, and while we believe we can see the finish line, there’s still room for MCC to spin out or reverse before this is all over.

Management – as well as the “activists” and would-be buyers who were pumping out press releases with abandon a few months ago – have all gone quiet.

The BDC itself has not issued a shred of disclosure since the news of the failure of the “go-shop” was announced last Monday.

Reading Material

Presumably the next major step is for the three Medley companies to issue revised proxies in advance of a shareholder vote.

That should be much more revealing and we’ll be reading whatever gets published and reporting back.

We’ll be curious – amongst other things – how none of 27 interested parties who signed non-disclosure agreements could offer better terms than the universally derided three way merger into Sierra Income ?

Is this a matter of the “eye of the beholder” or an objective fact ?

Main Road

Getting back to the week that just was:

Seven BDCs are now trading within 5% of their 52 week high, up from five the week before.

However, thanks to MCC, there are five within 5% of the 52 week low.

Lower Level

That list includes BlackRock Capital (BKCC), which we discussed last week, as well as PennantPark Floating Rate (PFLT), PennantPark Investment (PNNT) and Oxford Square (OXSQ).

We Go Together

Unfortunately, the twin PennantPark BDCs are both in the dumps at the same time partly because of a policy of jointly investing in certain credits.

That certainly saves the manager of both entities from having to go and find as many transactions to book but when the portfolio companies involved head south, so can the stock price of both lenders.

In this case both PNNT and PFLT are invested in Hollander Sleep Products, which filed for bankruptcy a few months ago, and which we’ve covered in the BDC Credit Reporter.

The two BDCs have committed $34mn to Hollander, and had to write down their debt by over (50%) so far.

Hollander is PNNT’s only non accrual and one of three remaining at PFLT.

Of course, there are other factors dogging both BDCs stock price but this “share and share alike” policy does have a downside when things go wrong.

Other Co-Investors

Nor is the PennantPark organization alone. The Gladstone Companies (GAIN and GLAD) often share investment exposure, as does Solar Capital.

Also very much in the habit of co-investing in this way is the FS-KKR organization.

When non-listed FSIC II merges with several other private BDCs managed by the KKR-FS Investment group – and goes public as planned – expect to see much portfolio overlap.

For investors who seek non-correlated BDC investments this can be a problem, while others may not care.

Some investors may be delighted that the asset manager can – in some cases – “control” a loan by doubling or tripling up with sister entities.

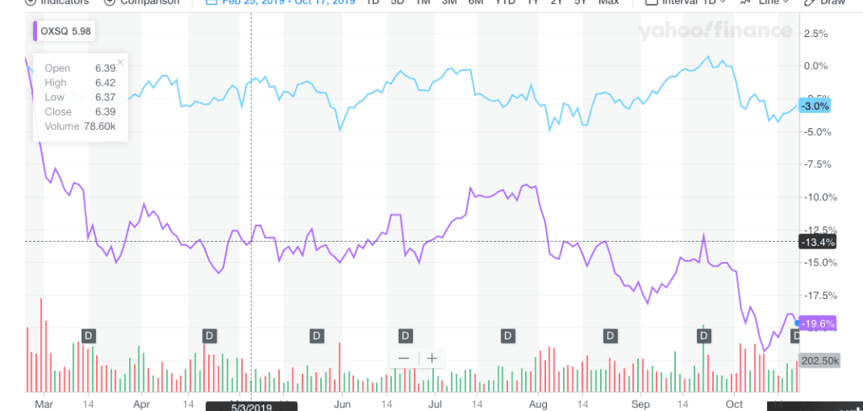

Hammered

Poor old OXSQ’s stock price has been dropping ever since February 22 – coincidentally when the BDC sector hit its apex for 2019.

The stock is down (20%), faring far worse than the sector as a whole, as measured by BDCS, as this chart shows.

We’re guessing investors are concerned about the state of the CLO market – facing lower LIBOR; potential higher credit losses and still narrow spreads.

Doubts may be rising about the ability of the BDC to maintain its $0.804 annualized distribution, even though its latest Net Investment Income Per Share was well above its pay-out and there are no non accruals.

OXSQ yields a juicy 13.6% – often a sign of market concerns – but is far from the highest out there.

We count 5 BDCs with higher yields.

One Month Out

Although, the BDC sector – and most of its components – had a good week, if we look back over the past month, we see more red than green.

By our numbers – shamelessly copied from Seeking Alpha – 29 BDCs are lower in price as of Friday compared with a month before, versus 17 that are up.

Also, since the BDC high point of February 22, only 13 are higher in price and 33 are down.

Looking Forward

If BDC stocks as a group are going to make a sustained move upward – rather than oscillate in a narrow band – good news from both the broader markets and from earnings season will be required.

We’re only two weeks away from the first rush of results.

This week we continued to add content to the BDC Earnings Preview with articles regarding TCG BDC (CGBD) and Fidus Investment (FDUS).

We’d have done more but were distracted by the release of Saratoga Investment’s (SAR) actual quarterly results, which close out in August.

The BDC performed well, both from an earnings and credit standpoint and seems dedicated to continuing the growth of its balance sheet, all of which we discussed on October 14.

Peek

FDUS, due to regulatory rules relating to the issue of a new Baby Bond, opened its kimono for the third quarter a little bit in a regulatory filing.

As we noted in the Earnings Preview for the BDC, recurring earnings seem to continue to be challenged but book value appears to have increased after taking a downward dive last quarter.

Both these BDCs give us some inkling of the sector’s general direction but not much.

Last. Not Least.

Over at the BDC Credit Reporter there were a handful of developments that might affect certain BDC’s future results.

Gas Leak

Ferrellgas Partners – a major investment of TPG Specialty (TSLX) – reported both very mediocre quarterly results and a dispute with the BDC, which serves as the administrator of its secured Revolver.

TPG Specialty says Ferrellgas – a major propane distributor and a public company – is in default. Ferrellgas says no.

Something has to got to give.

TSLX has $82mn outstanding in its loan so shareholders might want to pay attention, but we expect the BDC – master of the difficult credits – will be OK.

Unpaid

Coal miner Murray Energy is in forbearance mode with its lenders – including 6 BDCs but only one public one: FSK – and seems headed to bankruptcy court.

There’s $52mn at risk and $5.6mn of investment income at risk of interruption/loss, but “only” $19mn of the debt is held by FSK.

Branded

Another hot spot where something is likely to happen sooner rather than later is Sequential Brands.

There BDC exposure is huge: $292mn and first lien, second lien and equity.

The company is looking to sell off some or all of its assets or any number of other options to improve its dire, overly-leveraged status.

Two public BDCs: FSK and Apollo Investment (AINV) are involved, with $61mn and $13mn of exposure respectively.

Wider Context

In the broader leveraged debt markets, the trend is towards higher credit losses and more and more weaker performing borrowers trading at ever bigger discounts to par.

Here’s a report from S&P Global Credit:

|

Elsewhere, a global credit outlook survey of more than 100 financial institutions in 20 countries yielded negative expectations for credit performance:

|

True. But.

However, there’s no sign yet of a systematic and universal deterioration in credit conditions.

More of a drip, drip of weaker credit results and a heightening of concern, which meshes with our own view of what’s happening – albeit on a more accelerated basis – in the BDC sector, where risks are higher.

From Our Database

We’ve identified – so far – 274 under-performing BDC portfolio companies with an FMV of $8.9bn.

That amounts – and we’re speaking in very rough terms here – to about one-twelth of all BDC investments outstanding.

The number of under-performers is higher than most investors would prefer but not egregiously so.

Unequal

More worrying for some BDC investors is the huge variation amongst different BDCs.

Using the BDCs own portfolio rating systems for the June 2019 ended period, the range of under-performing investments as a percentage of all investments in a BDC goes from 1.1% to 32%.

Worryingly, there are 7 out of the 31 who report such information whose under-performing assets are greater than 30% of the total.

Another 10 BDCs have under-performers in the 10%-30% range.

That means more than half the BDCs reporting the valuations of their portfolio have a material proportion of their investment assets under-performing.

Capital Impact

We’d be remiss if we didn’t mention that the numbers are a little more worrying when compared with the net assets of the BDCs involved.

With ever increasing AUM funded by higher leverage – rather than equity capital raising – the potential damage to net asset values is increasing.

At the highest/worst level, under-performing assets account for 95% of net assets.

19 BDCs have under-performing assets greater than 10% of their net assets.

Positively Speaking

Of course, the standards for what is termed “under-performing” varies by BDC and there is always the possibility that troubled companies will turn around.

Nor does under-performance or even bankruptcy necessarily result in material losses as many BDCs – like TSLX where Ferrellgas is concerned – have senior debt status and protections.

The Other Side

Unfortunately – and speaking anecdotally – there have been very few instances of late where we’ve seen under-performing companies make a round trip back to performing status.

Furthermore, when we look at realized losses that have occurred – the best time for a final accounting – there have been plenty of instances of complete or almost complete write-offs, and very low recoveries.

For example, Investcorp Credit Management (ICMB) took a realized loss in the IIQ 2019 of ($22.0mn ) on Trident USA, essentially all its investment.

We’ve previously discussed the 100% unrealized write down (soon to be formalized into a realized loss) that Fidus Investment (FDUS) incurred where Oaktree Medical Centre was concerned.

Cost To Value

One other statistic that also causes us concern about recoverability of under-performing assets is the wide gap – in some cases – between the cost basis of non accrual loans and their reported FMV.

Non accruals are just one step away from realized losses and gives us some insight into how much of a troubled dollar might be rescued.

Very damning in this regard are the numbers for Ares Capital (ARCC) at June 2019, but which will serve for the sector as a whole.

According to its 10-Q, non-accrual assets at the BDC giant were 2.3% of total investments at cost but only 0.2% at fair market value.

That implies that ARCC expects to recover less than 10% of its non-performing investments…

Watching Out

Credit losses are part of the natural order of things where leveraged lending is concerned.

However, investors cannot afford to be complacent.

A bad run of credit reverses can effectively destroy a BDC’s value regardless of how well management handles all other aspects of the business.

Long term investors will remember the fates of American Capital, Allied Capital, MCG Corporation, Patriot Capital and GSC Investment before Saratoga

Even amongst the 46 public BDCs that remain in business today 19 – roughly 40% – have incurred losses equal to at least 25% of their equity capital raised.

OHA Investment (OHAI) – being rescued by Portman Ridge (PTMN) any day now – has lost a record (84%) during its run under two external managers.

MCC is at (65%).

PTMN itself – which racked up major losses when being known as KCAP Financial – has lost (55%) of the equity capital raised for the business.

Eyes Peeled

The BDC Reporter will continue to report weekly on what’s happening to BDC prices and trends.

However, we’ll also report frequently on changes in credit, the most important factor in the long term success of both individual BDCs and the sector as a whole.

.png)