Becalmed

Merged

The biggest development was that Golub Capital (GBDC) – after what seemed an eternity – received shareholder approval to merge with its non-traded BDC sister company: Golub Capital Investment Corporation.

Judging by the investment assets being combined and the track record of the external manager, we’d be surprised if there were any disappointments up ahead.

Pay Out

Otherwise, a couple of related BDCs (PennantPark Floating Rate – PFLT – and PennantPark -PNNT) announced monthly and quarterly dividends that were unchanged from prior periods, and as expected. (The credit troubles at the PennantPark BDCs that have hammered their stock price has not yet translated into affecting their distribution levels).

Also announcing distributions were Solar Senior Capital (SUNS) and Monroe Capital (MRCC). There, too, nothing unexpected occur.

SUNS announced its pay-out for September 2019 of $0.1175, unchanged since the third quarter of 2012.

MRCC’s $0.35 quarterly dividend has been the same now for 23 quarters.

All this activity is chronicled in the BDC Reporter’s Dividend Outlook Table for readers who want to review the big picture.

Lobby

In fact, the potentially biggest story of the week happened away from the markets at the SEC where a BDC lobbying group continued to demand change on the Acquired Funds Fees and Expenses (AFFE) rules.

Here’s how Reuters summarized the ticklish issue:

AFFE rules require investment companies and mutual funds investing in BDCs, which are a source of initial capital for small and medium companies, to include an additional line of expenses outlining the fees and operating costs charged by the BDC.

Though the SEC has argued that the requirement helps improve transparency in the market, BDCs have said it distorts expense ratios making them prohibitively expensive for a number of institutional investors that could have otherwise been attracted by the vehicles’ high dividend yields.

In its letter to the SEC, the CBD proposed that a BDC should be treated no differently than an investment in an operating company and that a BDC’s expenses should be included in a Statement of Additional Information (SAI) disclosure.

Under the CBD’s alternative proposal, a SAI disclosure would detail the BDC’s operating expenses. Any costs would be factored into the BDC’s trading price. The argument is that any expenses would be reflected in the fund’s total return.

The CBD said that within such a model it would no longer be necessary for the BDCs to be reported within a prospectus fee table and remove distortions in the expense’s ratio of an acquiring fund.

There’s no resolution on the immediate horizon, but analysts and pundits have previously contended that a favorable resolution to the AFFE rules would enlarge the BDC investor base; increase prices and improve corporate governance.

We’ll report back next time we hear anything material, but this subject has been in the BDC ether for many, many quarters so handicapping the timing of a resolution is well nigh impossible for those of us outside of the governmental beltway.

Broadly Influenced

The S&P 500 was up 1.79% on the week, after being up 2.79% the week before.

For The Week

The BDC sector – as measured by the UBS Exchange Traded Note which includes most of the public funds – with the ticker BDCS was up 0.28%.

The Wells Fargo BDC Index, which provides a “total return” increased 0.56% to reach a new 2019 YTD high. So far the WF Index is up 18.1% in 2019, but most of that gain (85%) occurred in the first 7 weeks of the year. Since February 22, 2019 any increase in the index has come from distributions rather than price movement.

As to the rest of our regular metrics: Two thirds (30 of 46) of individual stock prices were up or flat and one third (16) were down. Three BDCs went up 3.0% or more in price on the week.

One was OHA Investment (OHAI), up 5.4%, as investors sharpen their pencils about the impending acquisition/merger into Portman Ridge Financial (PTMN). For what it’s worth PTMN was down (2.5%) this week.

Unclear

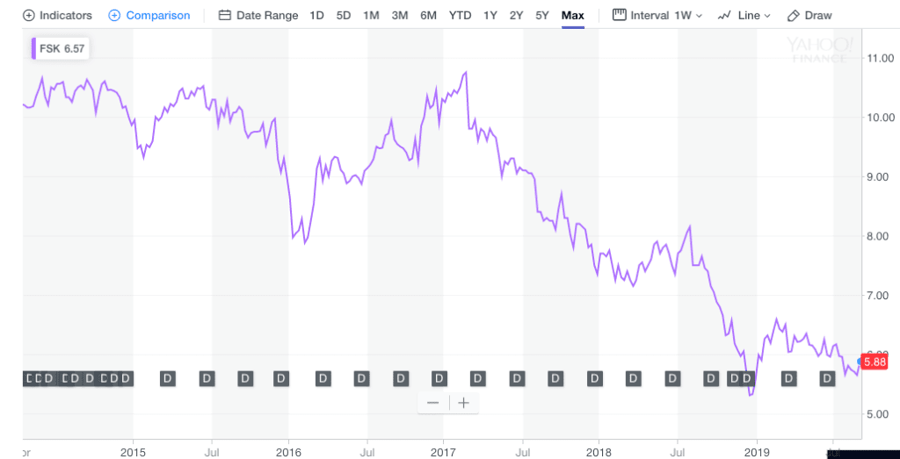

Also up what FS-KKR Capital (FSK): by 3.5%, to reach $5.88.

There’s no obvious reason why.FSK has been out of favor – despite its late 2018 merger with KKR-managed CCT Capital – from February 2017.

As this lifetime chart for FSK shows, the BDC fell out of favor back in February 2017 after reporting losses and in anticipation of a dividend cut that came shortly after.

In those two and a half intervening years, FSK has dropped 45% in price.

Since August 7, when FSK reached a low of $5.47, the stock is up 7.5%.The beginning of a price turnaround or just a blip before a further descent ?

Yet another reminder of both the wide variance in BDC prices depending on financial outcomes and how difficult it is for investors to guess right as that two and a half year downward slope illustrates.

Regular Feature

Speaking of the difficulty of guessing right, Medley Capital (MCC) was up 3.5% as investors try to position themselves for what might happen next.

That’s all speculation at this point but by the end of the month the outline of the final deal will be known and the BDC Reporter will have to find a new regular topic to update our readers on.

More Numbers

There were no BDCs dropping 3.0% or more in price this week. We did note, though, that the number of BDCs trading within 5% of their 52 week lows decreased by one, going from 4 to 3.

Still, we’re not making too much of this short term data.

In Between

The market remains in a state of limbo that’s been underway for months.

Three-quarters of BDC stocks remain below their February 22, 2019 level, when the sector peaked.As has been the case for some time, two-thirds of BDC stocks trade below book value – not a sign of much investor enthusiasm. 24 BDCs are trading above their 50 Day Moving Average and and 22 below. 20 BDCs are trading above their 200 Day Moving Average and 26 below.

All this – and other data we look at – suggests a BDC sector that is neither fish nor fowl; not rallying and not dropping, caught in purgatory.

.png)