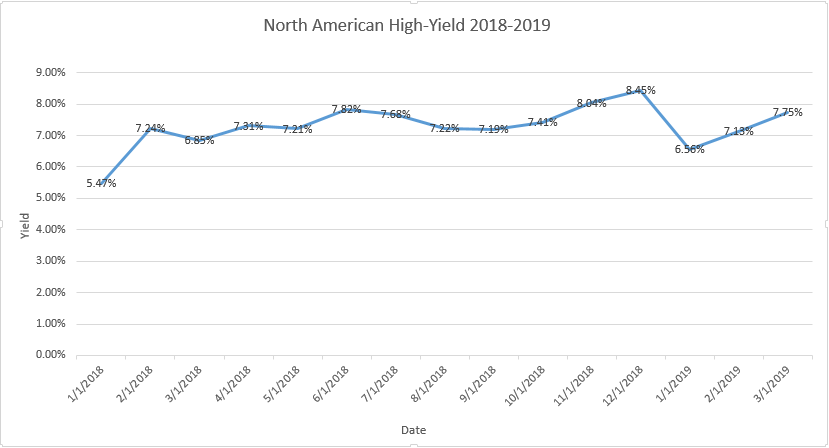

North American High Yield new issue average yields have been on the incline. Throughout 2018, a steady positive trend can be observed from January to November, when average yield peaked at 8.45%.

Volatility in December effected virtually all markets, as depicted in the North American High Yield average yield chart below. A sharp decline represents a drop in new issues average yield by almost two percent.

The new year has brought new growth to the High Yield space as average yield for North American High Yield new issues has steadily increased month over month.

Read More

Topics:

High Yield,

bonds,

junk bonds,

bond market

U.S. TREASURY YIELDS SLID ON MONDAY APPROACHING three-month lows as investors fled to safe-haven assets.

The 10-year benchmark settled near 2.857% losing 3.6 basis points while the inverted 2-year and 5-year Treasury yield gap

narrowed to .3 basis points.

Read More

Topics:

High Yield,

bond market,

market analytics,

Finance,

News,

research

Back in 2015, Marty Fridson, Chief Investment Officer at Lehmann, Livian, Fridson Advisors LLC, spoke with Barron's on the topic of high yield industries most sensitive to rising interest rates.

Read More

Topics:

High Yield,

junk bonds,

bond market,

market analytics,

YTW,

Fixed Income,

News,

interest rate

BDC COMMON STOCKS

Concession Speech

We are prepared to concede that the once semi-robust BDC common stock rally is in stall mode.

Read More

Topics:

BDC,

bond market,

market analytics,

business development company,

Fixed Income,

News

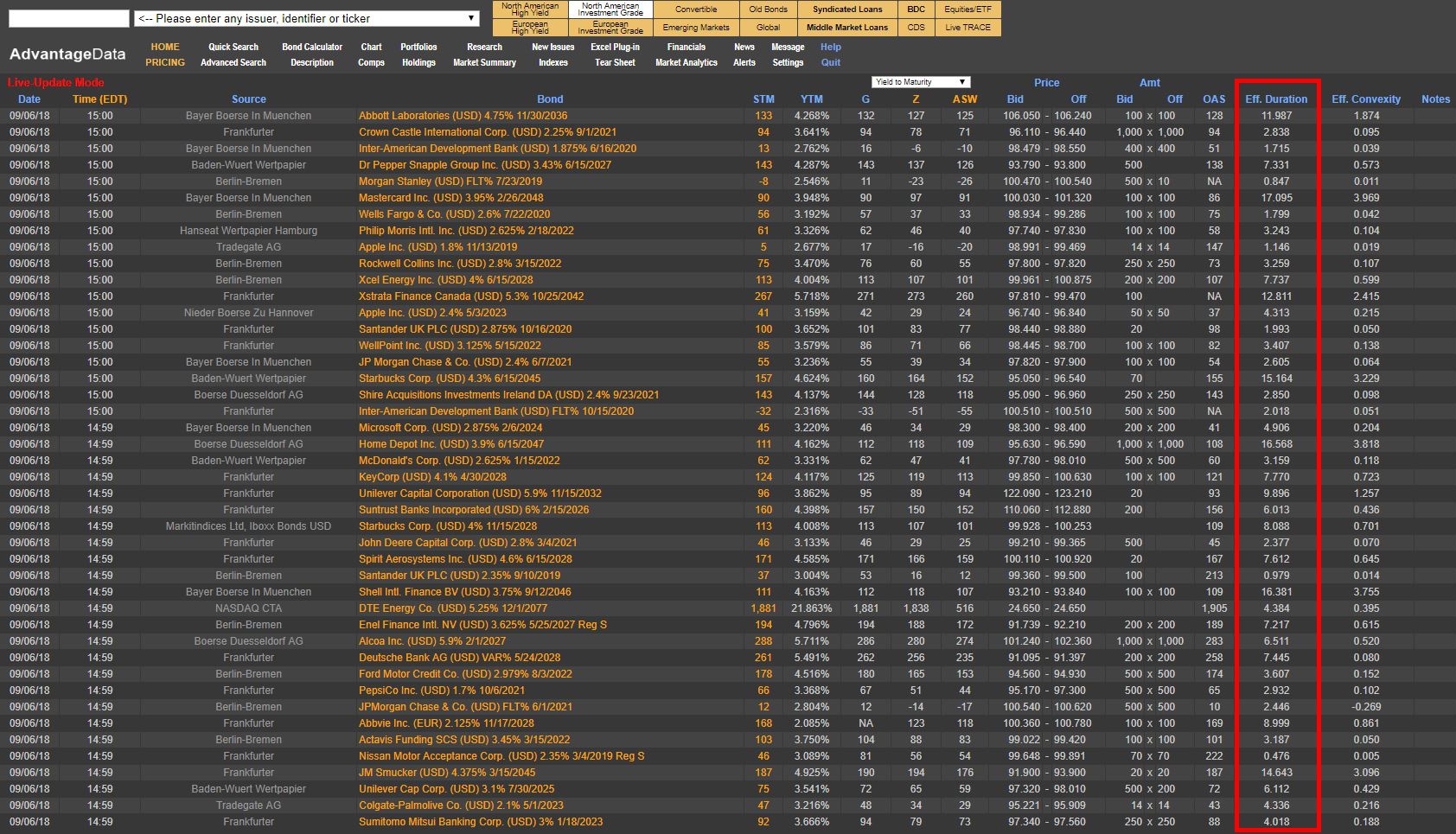

Duration risk has been a popular theme around buy-side firms as they look to incorporate low duration bonds into model portfolios to reduce interest rate sensitivity and increase liquidity. Typical bond indexes have an average duration of 5-7 years; this will create large outflow of assets in the upcoming quarters and increase popularity among individual securities.

Read More

Topics:

Investment Grade,

Analytics,

bonds,

Bonds Maturing,

bond market,

market analytics,

Fixed Income,

portfolio,

interest rate,

duration risk

.png)